Mader Group - A B2B Services Company in the Resource Sector

An analysis of a ASX: MAD business model

Disclaimer - Any information from the author is general only and has been prepared without considering your particular circumstances and needs. The nature of the blog is a reflection of the author’s personal experience and learnings. Please seek a licensed professional for advice.

So, I’ve decided to continue doing write-ups. However, I’ll emphasise this - all writing is for educational purposes only. I’m a finance and accounting student looking to pursue a career in the field. These public writings allow me to receive critical feedback from intelligent people, both professionals and private investors. This is an analysis of a public company and is not a recommendation to buy or sell any securities. At the time of writing, I do not own the company - but have in the past and may in the future.

This company is overlooked due to the cyclical reputation attached to the mining sector. In reality, it is a necessary operational expense for miners regardless of the commodity cycle and has historically shown healthy performance throughout the capex cycle, commodity price volatility, and industry downturns.

Mader Group ($MAD) is a leading contracting company in Australia that provides maintenance and repair services to equipment in the mining & resources sector. These services are specialised and technical, requiring a team of skilled tradesmen to provide a well-rounded offering. The business was founded by Luke Mader and IPO’d in 2019. Some quick facts about the business:

2,200 skilled employees

900+ support vehicles

480+ locations

350+ customers

9+ countries

Mining companies require equipment for day-to-day operations. Across its useful life, the equipment will require services, maintenance and repairs. Typically, the original equipment manufacturer (OEM) will provide support services for their equipment. However, they will only repair their own equipment which is a hassle for mine operators. They then have to deal with multiple OEMs to fix each piece of equipment. The OEM services are slow and expensive, as the sale of equipment is their bread and butter.

Mader Group fixes this problem. They offer a service that can support multiple brands and deliver the service faster and often at a better price relative to OEMs. There are other companies such as recruitment or temporary staffing businesses which may provide these services too, however, they lack the capability to provide an adequate service to larger clients. These staffing firms are cheaper but provide a subpar service when accounting for speed, breadth of service, quality workers, industry knowledge, etc. The mining companies would prefer to deal with a reliable, industry name with the capability to offer a well-rounded service for a reasonable price. It allows a single point of contact, rather than juggling multiple companies to solve issues on different equipment, requiring different trades across Australia or even internationally. Mader can provide these services to equipment from the mine sites extracting the commodities, all the way through to other verticles that mining companies have such as fixed infrastructure, electrical, rail maintenance, power generation, etc. The average client prefers worker quality as the main value-add. However, when clients are operating across many geographies in a specialised industry that requires unique skills and knowledge, they may weigh other factors alongside worker quality.

The company thrives due to its well-trained workforce, which is maintained by cultivating a quality work culture. It is vital for the business to attract, train, and retain employees as it’s the lifeblood of the business. They’ve implemented a ‘trade-up program’ focused on providing light vehicle and road transport mechanics with a tailored program to develop the skills necessary to become a qualified heavy-duty diesel mechanic, ready for placement into the mining industry. The program has seen 180 inductions since inception, with 122 active participants and 90% retention rate.

Mader benefits from increased production of commodities as it increases the operating time of machinery, leading to more maintenance requirements. Increased capital expenditures on machinery will provide more work for Mader in the distant future, but may temporarily hinder their demand in the short term as newer equipment is under warranty and operators will opt for OEM services. Currently, there is high demand for new equipment, however, manufacturers are struggling with supply chain issues in order to meet this demand. This forces operators to extend their use of existing equipment before replacement. Despite this capital expenditure cycle, Mader has displayed consistent growth over the past decade. The mining equipment during the peak capex expenditure in 2012 is now ~10 years old and requires more maintenance than ever.

The company started in Australia providing these services to sites in WA before expanding into other states in the next few years. Mader has been funding internal startups in the USA and Canada which have been rapidly growing in recent years. The business model has proven to work internationally across 9 countries with increasing demand for their services.

The capital-light nature of the business means the company requires little investment to expand operations, with most capex associated with vehicle fleets over fixed assets. Essentially all capex spend is growth and used on vehicle fleets.

This means the company is able to expand operations and spur organic growth with capital investments into vehicle fleets. The ROIC reflects effective capital allocation, generating attractive returns.

These are spectacular numbers, with return on equity often exceeding 30%+. However, they have been continuously declining in recent years which is something to consider.

The company still has the founder, Luke Mader, as the Executive Director in the business. The current CEO is Justin Nuich who took over from Patrick Conway in 2020, while Patrick continues to work in the business as the Executive Director of Emerging Businesses at Mader.

The majority of shares are held by insiders, totalling ~77% of the total share count. This is largely made up of Luke Mader (56.85%) and Craig Burton (19.5%), director at Mader and manages a venture capital firm. This has left a fairly illiquid market considering the size of $640m, with little institutional ownership. The long-term incentive plan is linked to NPAT in FY24 and FY26 targeting $40m and $60m respectively.

The company derives the majority of its revenues from Australia but has been accelerating its international footprint in recent years. In total, the company generated:

Australia: $40m EBITDA (+36% YoY)

North America: $10.1m EBITDA (+107% YoY)

Rest of World: $2.1m EBITDA (+49% YoY)

The company generated $402m in revenues and $28m in NPAT during FY22. Management has announced guidance for FY23 at $501m revenue and NPAT of $33m.

The growth drivers outlined by Mader Group:

Industry:

Total commodity/mineral production (requires more equipment + hours using equipment)

The average age of machinery (older machinery requires more maintenance)

Whether mining companies decide to outsource their maintenance

Mader Growth Strategies:

Being an employer of choice

Replicating the business model in new areas

Continuing to diversify by commodity

Maintain and develop customer relationships

Expanding the range of service offerings and markets (verticles - fixed infrastructure)

The total addressable market is extremely large allowing a long runway for future growth.

The revenues aren’t cyclical because they aren’t tied to commodity prices, but rather to production volume. These volumes are rather resistant to the volatility of commodity prices as miners continue to operate as long as they can cover their cost of production. In the case that a significant bear market occurs, mines may close shop. However, Mader group operates across a range of commodities around the world and provides services to some of the largest mining companies globally. This diversification and the ability to continue growing in other markets during market volatility creates resistance to commodity cycles.

In addition, the company has expanded past its focus on mobile equipment, growing vertically into other parts of the supply chain and other maintenance areas such as infrastructure, rail, electrical, etc.

There may be an inflection point in the near future due to the fast-growing NA segment outpacing other areas of the business. Notably, the margin in the USA and Canadian businesses are almost double the Australian segment with a 20% EBITDA margin.

The balance sheet is in a strong position with $26.7m net debt, totalling around 0.55x net debt/EBITDA. The business does not require much financing due to its ability to self-fund growth capex.

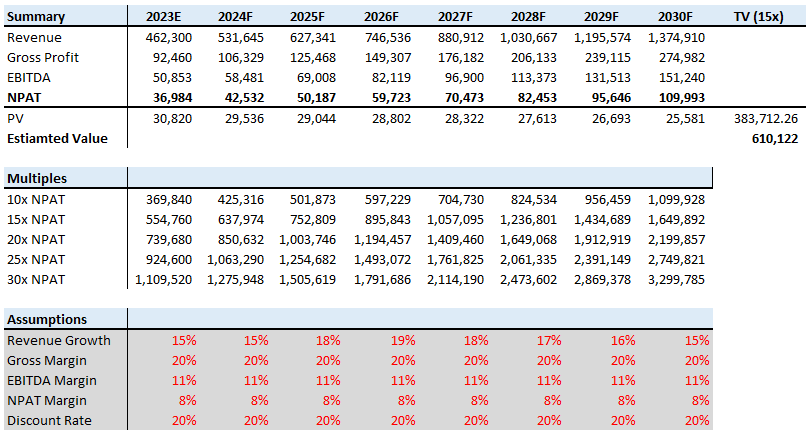

The business is likely capable of compounding revenues at around 15-20% over the long term. I’d assume normalised NPAT is around ~8%. Management is targeting $40m in FY24 and $60m in FY26 based on the long-term incentive plan.

The growth rates are arbitrary based on historical rates and hitting management incentive plans. Regardless, this scenario shows the range of potential valuations given the growth rates, 8% NPAT margin, and 15x terminal value. There’s also a reasonable case for margin expansion due to the improved economics in the NA segment. Management’s guidance of $33m NPAT puts the stock at 20x FY23 earnings. This is a fair valuation but is a bit too rich for my liking in the possible scenario that management is unable to execute their plan and underperforms as a result.

This leads to the risk for me, which is that the business is unable to hit its targets and the multiples contract. This may be due to being unable to recruit the manpower required to continue growth in a labour-scarce market, or simply over-optimistic expectations. The LTI targets for FY24 and FY26 provide a bit of comfort. There may be customer concentration risk, but find it unlikely that major clients would pull from Mader services considering the value that is offered relative to OEMs or smaller staffing businesses. Mader provides capability on demand internationally as a specialist in the field with a reputation for quality. The key to success in the business is the ability to attract, retain and upskill employees. If the company culture deteriorates and struggles to attract or keep employees, it may have a significant impact on business growth.

In summary, Mader has created a disruptive business model that holds competitive advantages over OEMs and temporary staffing businesses. This has been proven across Australia and recently found success in USA and Canada. The company looks capable of organically growing 15-20% p.a. into the medium/long-term future, paying out 20-30% dividends, generating 20%+ ROIC, and trading at 20x FY23 earnings.

If you’d like to connect feel free to reach out:

Email: investdoyle@gmail.com

Twitter: @investdoyle

Thanks for reading.

Great writeup Jacob. You did touch upon it, but do you know the reason for decline in ROE/ROIC in recent years? Even if you don't know the exact reason, would be interested to hear your thoughts about potential reasons for this decline.